Trump's election removes recession risks and anchors the "Higher for Longer" US rate scenario on the intermediate and long curves

Michael Israel, President of IVO Capital Partners, shares his view on the possible market consequences of Trump's election

The strength of the US economy and Trump's policies are reviving the scenario of persistently high rates.

Between opportunities and tensions: an overview of impacts

On the rates front

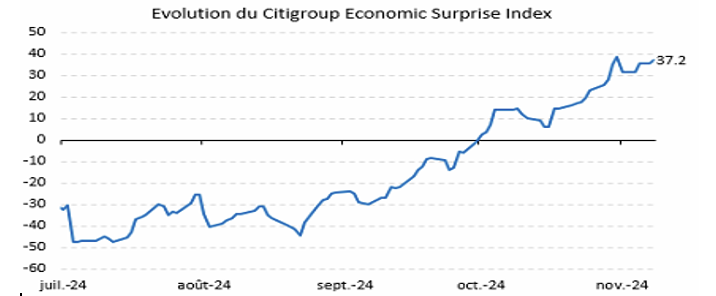

The intrinsic strength of the US economy, which has beaten expectations on most of the economic indicators tracked in the Citigroup Economic Surprise Index (Chart 1), alone justifies the recent rise in rates, while the election of Donald Trump reinforces this scenario.

Chart 1: Citigroup Economic Surprise Index from 01/07/2024 to 08/11/2024

Source : Bloomberg

The Citigroup Economic Surprise Index represents the sum of the differences between official economic results and forecasts. If the sum is greater than 0, economic performance is generally better than market expectations. If the sum is less than 0, economic conditions are generally worse than expected.

Its pro-growth policies support the extension of the economic cycle, but also raise fears of inflationary pressures or, at the very least, a slowdown in disinflation, as well as potential risks of a reassessment of the risk premium on US Treasuries.

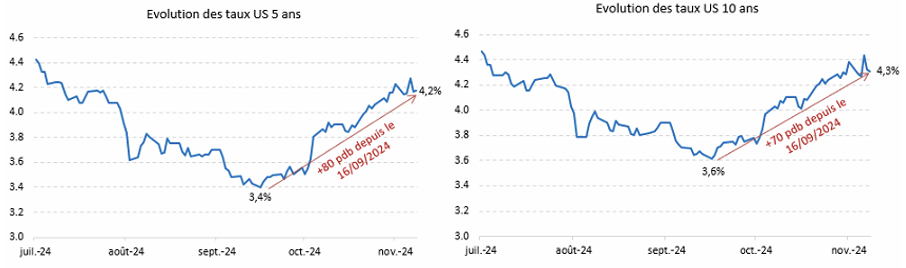

Chart 2: US 5-year and 10-year yields from 01/07/2024 to 08/11/2024

Source : Bloomberg

US 5-year yields: +20 bps between 05/11/2024 and 06/11/2024 following Trump's election (from 4.1% to 4.3%). Rates fell the day after the election to stabilize at 4.2%.

US 10-year yields: +10 bps between 05/11/2024 and 06/11/2024 following Trump's election (from 4.3% to 4.4%). Rates fell the day after the election to stabilize at 4.3%.

Since the Fed's pivot, the scenario of permanently higher US interest rates (higher for longer), particularly for intermediate and longer maturities, has regained momentum and is once again the reference scenario for many economists.

If this scenario is supported by the election of Donald Trump, some of his controversial measures, such as tariffs and migration restrictions, could exacerbate inflationary pressures and weaken the scenarios for key rate cuts, which for the moment are still expected to be based on 2 to 3 rate cuts in 2025.

Finally, combined with his promises of tax cuts, part of the market believes that these policies could almost mechanically push up Treasuries rates due to the worsening fiscal and budget deficit. A subject to be monitored in 2025, following what the "pragmatic" D. Trump would do in this context.

Equity markets

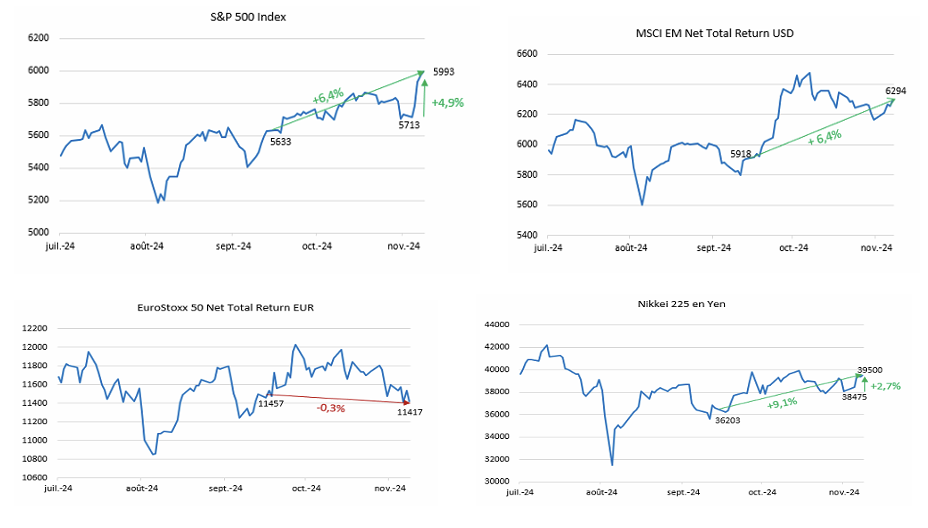

Equity markets: Risk-on sentiment despite rising rates

US equity markets continued to rise after Trump's election, reaching record levels, buoyed by expectations of an extended economic cycle, corporate tax cuts and the expectation of pro-growth policies. Emerging equities continued to climb post-election.

Source : Bloomberg

On the equity markets, the context of rising US borrowing rates already underway + the election of D. Trump is, for the moment, less welcome in Europe than in the emerging markets.

Corporate bond markets

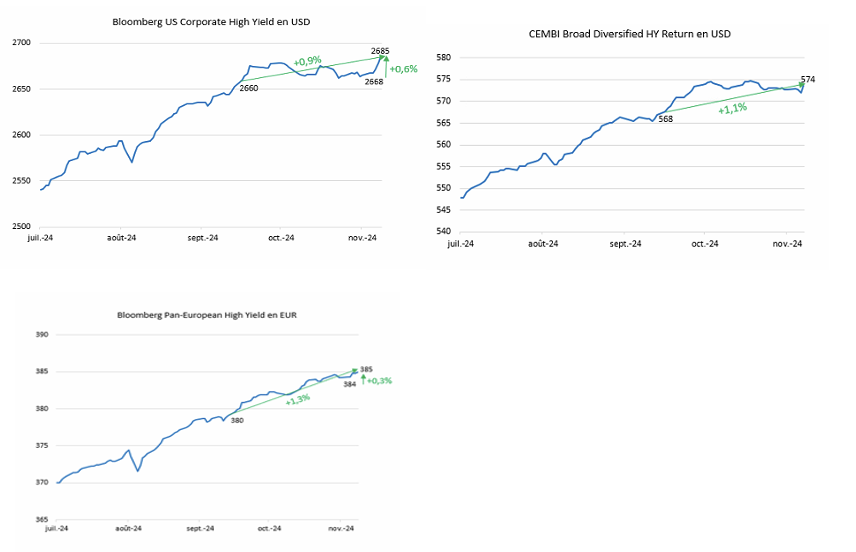

Credit markets (US HY, EM HY, Euro HY): Here too, "Risk-On" sentiment despite rising rates

Following on from the US equity markets, and for the same reasons, the US High Yield markets have risen despite the rise in interest rates since September 2024 and have continued to rise with the election of D. Trump.

This is also true of the emerging corporate high-yield market (CEMBI Broad Diversified HY) and the euro high-yield market, which have been on the rise since September and since the election.

Sources: Bloomberg & JP Morgan

Yields are rising, bond performance is positive, so credit spreads continue to compress across the corporate debt markets.

On the currency front

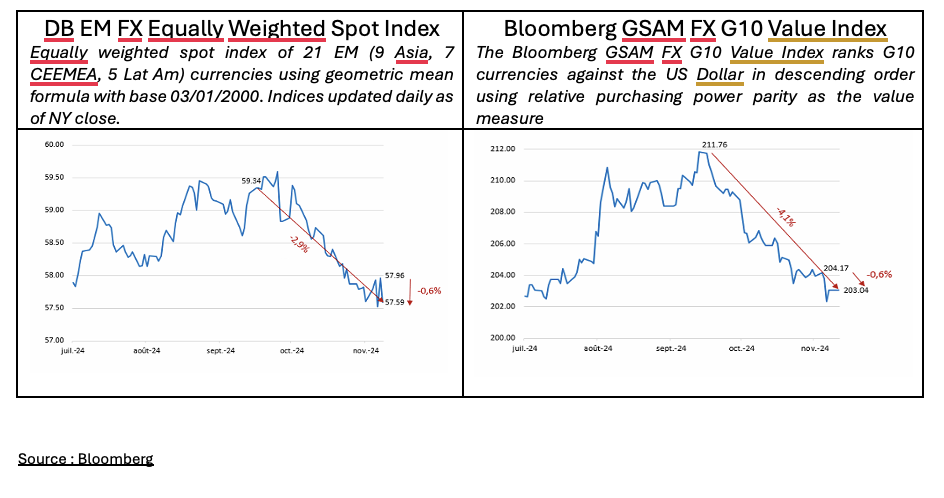

Currencies and emerging markets: resilience in the face of strong dollar pressure.

On the currency front, the dollar's appreciation seems inevitable, supported by a higher-for-longer scenario. For the time being, this repricing is taking place without any violent sell-off.

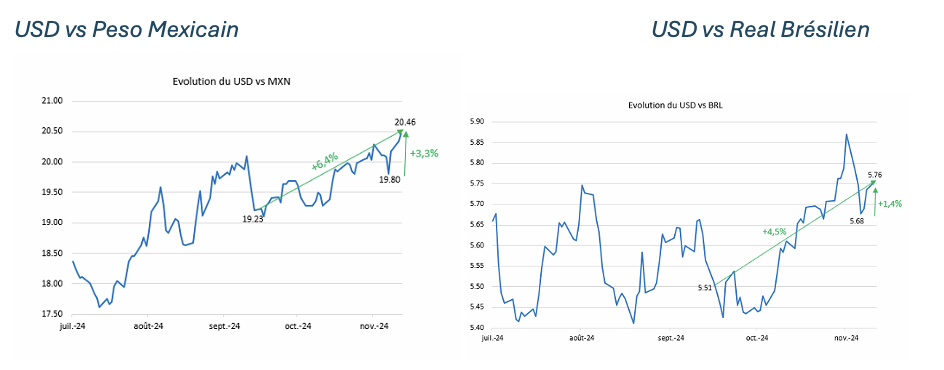

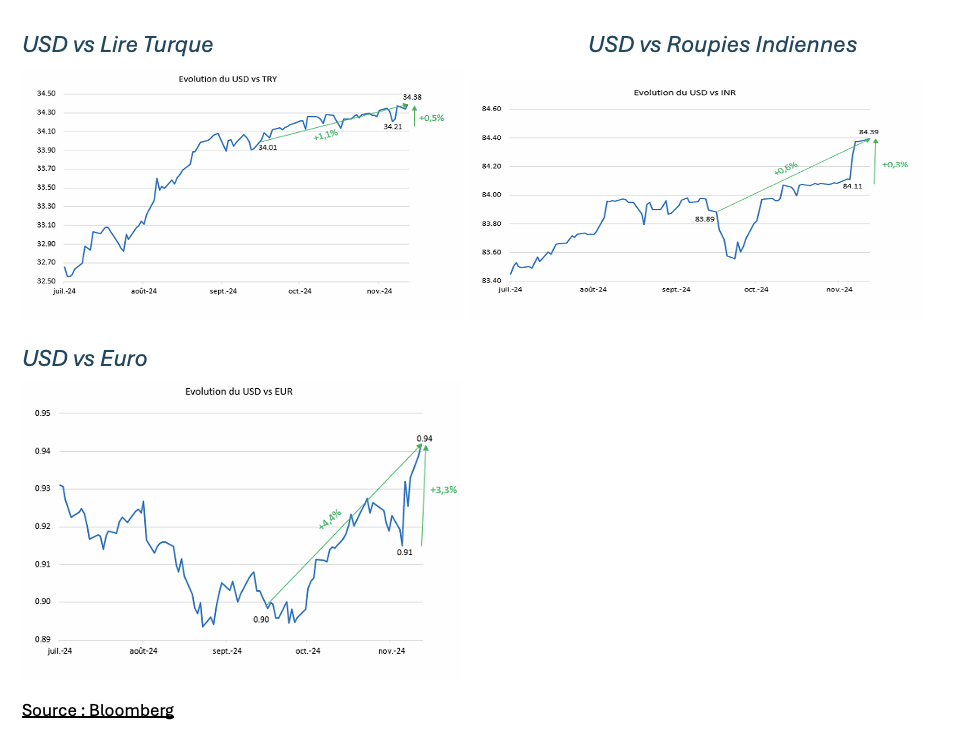

Example of a few currencies

The central banks of emerging countries, faced with resolutely positive US real rates, find themselves in a delicate position: a fall in their own local rates could accelerate capital outflows and too rapid a devaluation of their currencies, forcing some economies to adjust their monetary policy out of necessity rather than choice.

Although the dollar's rise complicates the situation for emerging economies, particularly those with USD-denominated external debt to service, it also offers opportunities for competitive devaluation, which strengthens their export margins - a valuable asset, especially in the event of increased US protectionism.

As with the equity markets, the currencies show a similar pattern: the euro and the G10 currencies seem to be reacting most negatively to the US 'higher for longer' scenario and the election of Donald Trump.

D. Trump's policies: what positive externalities are expected for emerging markets?

Geopolitical stabilization and growth: favorable factors for emerging markets.

In the media, Trump's policies are often perceived in an alarmist light, but it's important to examine their positive externalities. First of all, sustained US growth boosts global sentiment and economic momentum. Moreover, we should note that, in parallel, China is currently adopting ambitious stimulus measures, which will add an additional global growth engine. So, if D. Trump also manages to stabilize certain geopolitical zones, such as Ukraine and the Middle East, this could translate into a more favorable climate for emerging markets.

On a microeconomic level, one of the main risks lies in the pressure on the margins of exporting companies in emerging markets, due to potential tariffs. However, during Trump's first term in office, these tariff hikes were introduced gradually, which did not give rise to any major problems. In addition, a strong dollar can mitigate this effect, boosting these companies' export competitiveness.

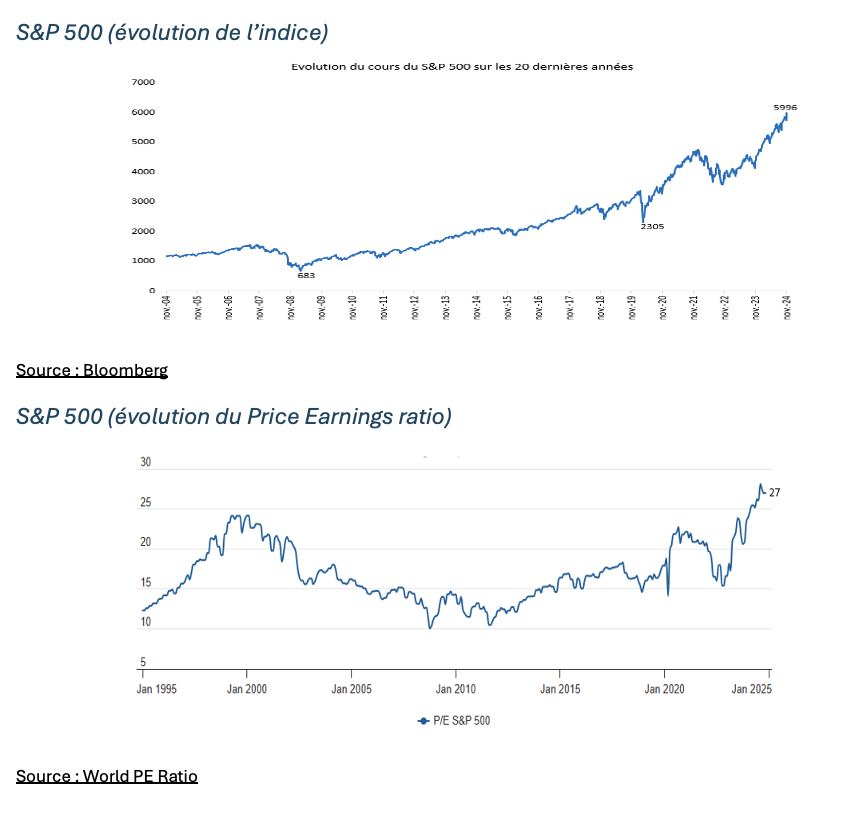

A dilemma between economic growth, rising interest rates and high valuations.

Faced with the dilemma between an extension of the US economic growth cycle ("no landing" scenario) and a rise in US interest rates (intermediate and long) and a strong dollar, US and emerging markets appear to have chosen sides for the time being: the election of Donald Trump increases the likelihood of an extension of the US economic cycle and reduces the prospects of recession.

However, the current difficulty lies in the high level of valuation of US and dollar-denominated assets, as this cycle extension takes shape.

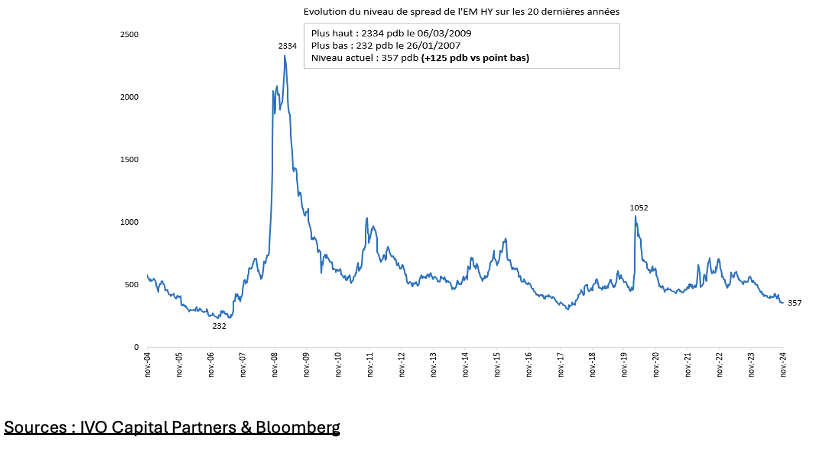

US High Yield credit spreads

Sources: IVO Capital Partners & Bloomberg

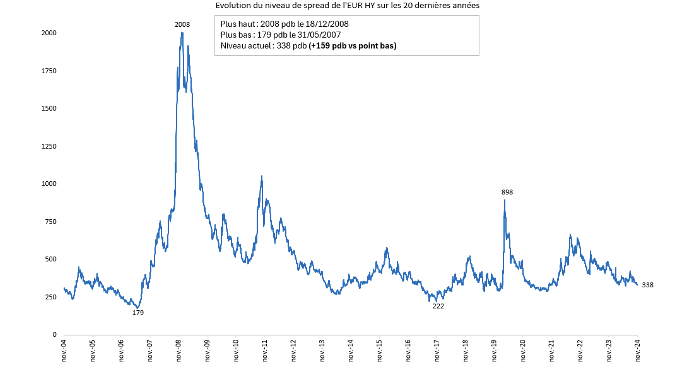

Euro High Yield credit spreads

Sources: IVO Capital Partners & Bloomberg

Current valuations: between good reasons and limited opportunities

In a context of high valuations, discipline is essential.

In an environment where asset prices are already incorporating the good news, it is essential to remain disciplined. In the US and emerging hard-currency HY corporate bond markets, the hunt for capital gains via spread compression from current levels is becoming less attractive. The good news is that a safer, more satisfying alternative is available to investors: USD carry.

USD carry on high-quality HY bond portfolios: a simple and effective alternative

With 5-year interest rates returning to 4.3% (and real rates close to 2%) combined with spreads of 357 bps, the 8% carry for an average BB rating in a context of sustained high rates (higher for longer) already represents a clear opportunity in its own right.

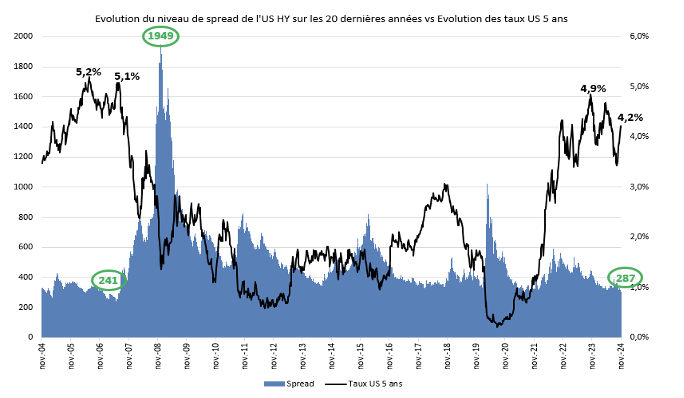

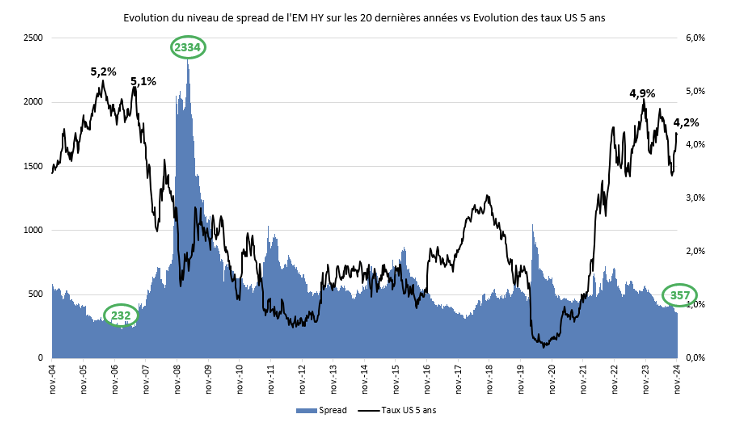

By remaining in the investment-grade High Yield segment, in addition to the carry, we also benefit from an option for potential spread compression in a scenario of perfect star alignment, as in 2007. Indeed, in this analysis of the potential for spread compression in international High Yield segments, it's worth remembering that in 2007, at the heart of a cycle of rising US key rates and the curve as a whole, that's when High Yield spreads reached their lowest level in 20 years. As today, this compression reflected strong investor confidence in the strength of the economy and in the ability of companies to meet their debts, despite a context of rising interest rates. An environment similar to the current one.

Sources: IVO Capital Partners & Bloomberg

This was also true of the USD emerging corporate bond market.

Sources: IVO Capital Partners & Bloomberg

While this potential spread compression may be beneficial for lower-quality High Yield assets (rated B and below), these lowest-rated assets also have high volatility, which we believe limits their appeal in the current environment.

A defensive strategy against a backdrop of potential volatility

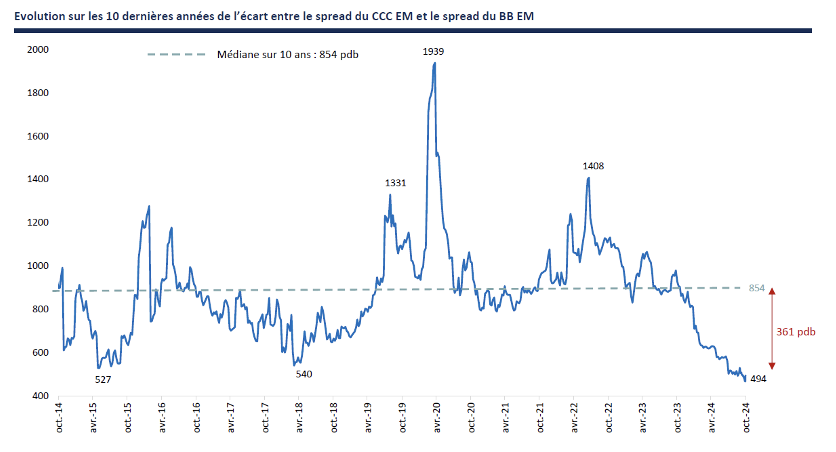

The high credit quality of our High Yield portfolio (rated double BB on average) is designed to ensure our resilience in the face of possible disappointments or changes in outlook. A key advantage of our current market configuration lies in the low risk of underperformance associated with a cautious approach, as low-quality bonds have already benefited from a significant rally. As mentioned above, the yield spread between CCC vs. BB bonds is currently at its lowest level in ten years, reducing the incentive to take on additional risk in terms of both on-board volatility and default risk.

Sources: IVO Capital Partners & JP Morgan

What's more, in our investment universe, the interest in turning to the lowest High Yield ratings lies mainly in "bad country/good company" opportunities - in other words, quality companies penalized by their country's sovereign rating. By way of information, almost 40% of the CCC-rated bonds in our index concern Argentine companies, which we know well at IVO and which are often of great interest. However, current average credit spreads for these Argentine companies are 346 bps (Chart ...), making the CCC segment of our investment universe less attractive, even for quality companies, than the opportunities offered in the BB segment.

Sources: IVO Capital Partners & JP Morgan

Our "defensive High Yield" positioning reflects our conviction that an offensive choice of ratings does not, in the current context, offer a sufficiently attractive risk/return ratio. High Yield, as a whole, seems attractive to us because of its level of carry, which is too advantageous to be abandoned at this stage, as well as its still-existing spread compression potential, reminiscent of the situation in 2007, although this is not our investment thesis. Drawing lessons from 2007 and its outcome, we have preferred to strengthen credit quality by moving more towards BB ratings, rather than seeking out the last mile of potential spread compression on increasingly expensive and volatile assets.

Given the uncertainties surrounding D. Trump's policies - tariffs or fiscal expansion, their economic effects (inflation or pressure on margins), their timing and the already high valuations - our "defensive High Yield" positioning seems particularly logical and appropriate to navigate in this context.

Our positioning in IVO EM Corporate Debt (ex IVO Fixed Income): "be well paid while remaining well positioned for future opportunities".

Faced with this new market configuration, we anticipated these dynamics by reducing the duration of our fund two months ago, taking profits thanks to lower rates and strengthening our positioning. Today, our flagship fund has a duration of 3.6 (versus 4.6 at the start of 2024) and 7% cash, offering the flexibility to seize opportunities that emerge with the rise in US rates that began in September. As US intermediate interest rates rise, not least due to potential "Trump volatility", we remain confident in reinvesting in high-credit-quality bonds and gradually increasing our duration, taking advantage of particularly attractive real rates. Our IVO EM Corporate Debt portfolio, with its predominantly BB rating, offered an attractive USD yield of 8.4% at end-October, representing a favorable risk/return profile in an environment more conducive to carrying than to seeking high mark-to-market capital gains.

Conclusion: High real interest rates due to sustainable growth: an optimal configuration for bonds?

Let's reiterate what we've been saying for several months: a "higher for longer" rate scenario in the US, supported by solid economic growth and positive real rates, represents one of the most favorable configurations for us as bond lenders.

As long as rates and yields remain high, we can reinvest our coupons on advantageous terms, without the risk of early redemption, thus optimizing our long-term return on investment.

As long as companies adapt to these rate levels, the situation remains objectively ideal for lenders, with a particular advantage for companies with low debt levels. In other words, a fall in rates is not the optimal path for high-performance bond investments; it brings rapid gains but less than the gains initially embarked upon, whereas a context of high rates maximizes profits over the entire duration of the investment.

If, however, the narrative around the strength of the US economy and the extension of the cycle were to change - potentially as a result of the "higher for longer" scenario (the economy operating as a cause-and-consequence loop) - our positioning in bonds with relatively short durations, mainly BB ratings, a protective annual carry over a full year, and a significant proportion of nominal and real rates in the overall yield, should help limit drawdown.

Disclaimer: All data presented in this note are sourced from IVO Capital Partners, Bloomberg and JP Morgan as at 08/11/2024. All investments entail risks, including the risk of capital loss. Returns shown are no guarantee of future performance.