Argentina's fiscal rehabilitation: first steps on a steep slope

Summary

- The country, previously in default, rekindled investor hopes with the election of a controversial libertarian president, Javier Milei. However, his ambitious fiscal program ran up against familiar obstacles, including political turmoil and corruption scandals, which quickly eroded investor confidence and once again dampened economic activity.

- Increased volatility followed the heavy defeat of Milei's coalition in the Buenos Aires regional elections, rekindling fears of a comeback by the Peronist movement ahead of the crucial October 26 legislative elections.

- Foreign exchange reserves remain a source of concern due to their increasing consumption to maintain an overvalued Argentine peso (ARS) within a predefined band. Unexpected support has come from the United States, however, with the announcement of a program including a USD 20 billion swap line designed to stabilize the exchange rate, but confirmation and further details are needed to reassure the markets.

- Even if Milei achieves a favorable result in the mid-term elections, his government will still face the challenge of finding an optimal balance of policies to control inflation and the exchange rate in order to consolidate its stabilization program.

- Despite the recent correction in sovereign debt, companies have remained resilient overall, bolstered by their export activities and solid credit profiles. Future volatility could offer emerging investors buying opportunities in corporate bonds.

Argentina's economic slowdown: from global prosperity to unprecedented decline

"There are four kinds of countries: developed, underdeveloped, Japan and Argentina. This remark, often attributed to Nobel Prize-winning economist Simon Kuznets, aptly illustrates the singular journey of Argentina, a country that was once among the richest in the world but later became an example of economic decline. At the beginning of the XXᵉ century, Argentina boasted a GDP per capita comparable to that of Europe and the United States.

However, in the middle of the XXᵉ century, this golden era began to fade. Political instability, marked by successive military coups and authoritarian regimes, combined with populist policies consolidated by the Peronist regime, led to an era of protectionism, excessive state intervention, fiscal mismanagement and hyperinflation. By the dawn of the XXIᵉ century, the country had suffered multiple defaults, including the catastrophic crisis of 2001 (the largest sovereign default in history at the time).

Milei and the economy: Argentina's radical turn towards fiscal austerity

Market expectations of Argentina changed with the election of Javier Milei, an eccentric economist and media personality, who defeated the Peronist candidate in the last presidential election, winning the run-off with anti-progressive rhetoric and a radical libertarian agenda. Milei took office in December 2023, brandishing a chainsaw at campaign rallies to symbolize his intention to drastically reduce

public spending. His unconventional style, combined with the difficulties encountered by Mauricio Macri during his term in office, raised questions about his ability to implement the promised austerity measures.

Nearly two years into his mandate, the President has been active with executive decrees and structural reforms. His measures have created short-term social hardship in exchange for long-term economic stabilization, eliciting a positive reaction from financial markets and positioning Argentina as a candidate for fiscal recovery. In 2024, Argentina recorded its first budget surplus in 14 years, and in July 2025, it obtained a credit rating upgrade from Moody's, the first in over a decade.

One of Milei's major successes was to bring inflation under control. This was largely achieved by ending monetary expansion as a financing tool and stopping the excessive money printing by the central bank (BCRA) that had fuelled hyperinflation. When he came to power, monthly inflation hovered around 25%; by May 2025, the consumer price index had risen by just 1.5%, the lowest level in five years. Annual inflation, which had peaked at 211.4% in 2023, fell to 33.6% in August 2025. This cooling, achieved without widespread social unrest or massive strikes, has helped restore some confidence in the peso.

As a result, Argentina abolished strict exchange controls, introducing a floating exchange rate regime for the Argentine peso (ARS). The Central Bank (BCRA) introduced a fluctuation band, intervening in the foreign exchange market when the spot rate approached the floor or ceiling. International reserves were bolstered by a USD 20 billion commitment from the IMF, and credibility was enhanced by the adoption of a fiscal discipline program. However, concerns intensified as the use of reserves increased to maintain the exchange rate at the ceiling, concerns only temporarily alleviated by the announcement of US support from Scott Bessent and Donald Trump on September 22, which could include a USD 20 billion swap line. Volatility resumed in the absence of confirmation or further details on this program, offering ARS holders a window to sell the overvalued currency. Meetings between senior government officials during the week of October 6, followed by a meeting between the two presidents on October 14, should provide important catalysts for market activity in the short term.

Economic growth has also rebounded from an initial contraction, with GDP expanding in 2024 and by around 6.0% in the first half of 2025. The recently presented 2026 budget forecasts continued solid growth while maintaining low inflation. Official projections remain more optimistic than market consensus, with economic activity slowing in the second quarter of 2025 - under the impact of political turbulence and monetary tightening

-, signalling a slowdown on the previous quarter and the possibility of a weaker third quarter.

Most of Milei's measures have been implemented by presidential decrees, many of which have been opposed by the judicial and legislative branches. With at least a third of the seats in Congress, Milei would be able to uphold his decrees and exercise veto power over parliamentary budget initiatives. In the future, its ability to negotiate ad hoc alliances will be decisive, as the backlog of structural reforms requires strong legislative support to produce lasting effects, particularly in the sensitive areas of labor, taxation and pensions.

Argentina's tax recovery: a difficult road ahead

The success of Milei's economic plan depends largely on the outcome of the October 26 parliamentary elections, in which almost half the seats in the Chamber of Deputies and a third of the seats in the Senate will be at stake. If his coalition wins at least a third of the lower house, Milei should be able to enforce his vetoes and decrees. However, to push through unpopular but crucial long-term reforms, notably in the pension and social sectors, broader support will be needed.

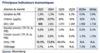

Concerns about the legislative elections increased after the September 7 elections in the province of Buenos Aires. Amid a corruption scandal involving Milei's sister, the president's allies suffered a crushing defeat, with the center-left coalition securing 47% of the vote to Milei's 34%. These results were partly influenced by a low turnout (63%), with some voters abstaining in protest against a government that had promised to fight corruption, while the left-wing candidates succeeded in mobilizing their base. In 2023, Milei had enjoyed strong support from young voters, who will remain a key demographic group in the parliamentary elections.

Milei's popularity plummets after corruption scandal

Presidential election results and voter profile

Since then, Milei has adopted a more conciliatory tone and accepted the defeat of his allies, contrary to his initial inclination to discredit unfavorable results. He has presented the 2026 budget with provisions to strengthen governability, taking into account both the short term and the October 2027 presidential election. Buenos Aires governor Axel Kicillof emerged as a key center-left candidate after his camp's strong performance in the province.

The negative market reaction underscores fears of another setback for Milei. However, a few factors, such as a higher turnout, a more right-wing electorate outside Buenos Aires and recent initiatives to engage centrist politicians, provide food for a more constructive view. The risks remain significant, particularly if Milei's popularity were to deteriorate further as a result of social unrest or new corruption scandals involving his allies. While disenchantment may not necessarily divert his electorate towards his rivals, it could once again contribute to low turnout in an electorate known to be highly sensitive and reactive.

Investment opportunities

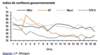

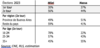

Recent volatility has pushed sovereign spreads to new highs, reaching around 1,300 bps (+540 bps) in mid-September. While sovereign bonds remain more volatile due to the political context, corporate credit has held up better. The corporate bond index widened by around 70 bps to a peak of 497 bps, and currently offers an attractive yield of 8.5%. We believe that this volatility may offer opportunities for solid issuers with a defensive profile in the face of the main risks facing Argentina, including :

- Exporters of natural resources. Argentina is one of the world's leading producers of agricultural products such as soybeans and corn. In addition, oil and gas producers have benefited from increased production and improved cost efficiency in the Vaca Muerta fields, providing an additional source of foreign exchange earnings.

- Local companies with strong credit profiles. Despite their exposure to the domestic economy, some companies are well positioned to withstand Argentina's volatility. These companies occupy leading positions in their markets and have historically posted good results while maintaining healthy balance sheets.

Argentine corporate bond spreads compare with 262 bps for the Latin American corporate benchmark and 360 bps for the global emerging market high yield corporate bond index. While the asset class as a whole may benefit from positive catalysts, the strong fundamentals of some companies limit the downside risk while offering an attractive carry relative to their risk-weighted level.

Sovereign volatility

Corporate loans holding up better than sovereigns

Conclusion: outlook for the weeks ahead

As one of the world's most frequent sovereign defaulters, Argentina faces a difficult and demanding path to fiscal stability and restored investor confidence. If Milei can successfully overcome the political and fiscal hurdles ahead, his program could consolidate Argentina's economic stabilization. October's legislative elections will be a key test, closely watched by the markets.

While the outlook for an improved fiscal environment is positive and an important catalyst for corporate performance, some companies with strong credit profiles also offer limited risk in the event of unfavorable electoral outcomes for the market.

DISCLAIMER THIS DOCUMENT DOES NOT CONSTITUTE FINANCIAL ADVICE:

The information provided reflects the opinion of IVO Capital Partners at the date of this publication. The information contained herein is not intended to be understood or interpreted as financial advice. It is shared for information purposes only, does not constitute advertising and should not be construed as a solicitation, offer, invitation or inducement to buy or sell securities or related financial instruments in any jurisdiction whatsoever. CONFIDENTIALITY NOTICE: The information contained herein is strictly confidential and may not be reproduced, redistributed, disclosed or transmitted to any other person, directly or indirectly. It is forbidden to copy, reproduce, distribute, publish, display, modify, create derivative works from, transmit or exploit this content in any way whatsoever, to distribute any part of it over any network, including a local network, to sell or offer it for sale, or to use it to constitute a database of any kind whatsoever.

IVO Capital Partners │Société par action simplifiée au capital de 250 000 € │Head office: 32 Rue de Monceau, 75008 Paris │ 753 107 432 000 35 RCS Paris │N° TVA : FR 54 753107432