Focus on primary market trends and prospects in emerging countries

"The primary market for emerging market corporate bonds plays a central role for our asset class. During the period of global monetary tightening, activity in the primary market has slowed significantly in recent years. However, the start of a rate-cutting cycle in the US should encourage issuers to return to the markets to refinance their existing debt on more favorable terms, and to extend the maturity of their bonds. Despite an expected rise in new issues ahead of the US presidential elections, we believe that the market's solid fundamentals will enable it to absorb this increase in new bonds."

Jeremy Landau, Senior Analyst, IVO Capital Partners

IVO Capital Partners' long-term vision

- Bond issuance rebounds in emerging markets: After a long period of global monetary tightening, the primary market for emerging market corporate bonds is set to rebound in 2024 thanks to a number of favorable factors, including the start of interest rate cuts in the US, which will offer issuers opportunities to refinance their existing debt on more attractive terms than before.

- Regional divergences in issuance trends: Turkey is leading issuance growth in the Central, Eastern Europe, Middle East and Africa region, stimulated by the disparity between high local rates and lower USD borrowing costs. Conversely, China, despite its status as a major issuer, is moving towards domestic financing and has seen its overall issuance decline.

- Impact of lower U.S. interest rates: The U.S. Federal Reserve's rate cut should lead to an increase in new corporate bond issuance in emerging markets, as issuers take advantage of more favorable borrowing costs, particularly in Latin America and Asia, where demand for financing remains strong.

- Favorable market conditions for investors: Despite the increase in bond issuance, solid market conditions, supported by negative net financing and strong investor demand, suggest that the market will naturally absorb this new supply.

Introduction

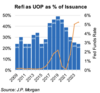

In 2024, the market for new corporate bond issues in emerging countries is evolving in a complex environment offering growing opportunities, and marked by a subtle but important shift in risk management and capital allocation. After a long period of global monetary tightening, the Fed's first interest rate cuts have introduced a new dynamic, creating more favorable issuing conditions for emerging market companies. This adjustment offers issuers the opportunity to access a market where the cost of capital, while still high, is beginning to fall. The total cost of borrowing for issuers is currently lower than in 2022-2023, thanks to reduced risk-free rates and lower spread premiums. Investors' search for yield, combined with issuers looking to take advantage of the Federal Reserve's policy change and enter the market before the period of uncertainty likely to be caused by the upcoming US elections, has led to an acceleration in bond issuance efforts. As a result, September promises to be one of the busiest months of the year. J.P. Morgan expects emerging market corporate bond issuance to reach $340 billion in 2024, up 40% year-on-year, the highest level since 2021.

Taking a closer look at recent developments, we'd like to highlight a few interesting trends we've observed in the primary market for emerging bonds.

Favourable market dynamics

Despite the sharp increase in new issues in September, we are convinced that the overall market outlook remains positive. The increase in new issues, which has already exceeded 2023 levels, has been absorbed by a market supported by negative net financing (taking into account maturities, coupons and tenders) and strong demand from local, emerging market and crossover investors. In terms of region, CEEMEA (Middle East, Eastern and Central Europe, Africa) is leading the way in the primary market this year, and is poised to set a new issuance record. Conversely, China, although still the world's largest issuer, remains well below the record levels of previous years.

Turkish issues rebound: divergences between local and US rates encourage foreign issues

The main contributors to the CEEMA (Central, Eastern Europe, Middle East and Africa) region's record primary issuance in 2024 are Turkish new issues, which have rebounded to their highest levels, exceeding market expectations and already doubling 2023's figures with $13.9 billion of issuance to date. Corporates have issued $6.1 billion, while banks have contributed a further $7.8 billion. Turkey is a good example of how emerging market corporate bond issuance can be stimulated by the divergence between lower USD interest rates and persistently high local rates. With the easing of monetary policy by the US Federal Reserve, dollar borrowing costs are

have become more attractive to Turkish companies, especially compared with high domestic interest rates (with 5-year and 10-year government bonds at 30% and 26% respectively). In addition, the need for Turkish companies to refinance existing debt and finance new investments in a gradually stabilizing economic environment is also stimulating increased issuance.

This momentum is also being driven by the appetite of foreign investors for higher yields on Turkish bonds, which is being supported by an improvement in market sentiment due to Turkey's efforts to implement more orthodox economic policies. Consequently, the combination of lower USD borrowing costs, a high local interest rate environment and growing interest from international investors has led to this rebound.

Chinese companies remain the main issuers in emerging markets, but represent a much smaller share of the market

Chinese companies have historically dominated bond issuance in emerging markets, accounting for 44% of it at its peak in 2018 with over $200 billion in new issues (according to J.P. Morgan). Although still the largest issuer in emerging markets since the start of the year, China now accounts for a much smaller share of the market, limited to Investment Grade issues often placed in the domestic market.

The slowdown in Chinese corporate bond issuance can be attributed to a number of factors, including persistent difficulties in the real estate sector and more attractive local borrowing opportunities. The real estate market, a key driver of China's economic growth, has suffered

very high debt levels, defaults and declining demand, reducing investor confidence and limiting the ability of real estate companies to raise funds through new USD bond issues. At the same time, Chinese companies are increasingly turning to domestic financing channels, such as bank loans and local bond markets, which often offer more favorable terms thanks to government support. To put this in perspective, local Yuan issuance in 2024 is expected to reach $1.3 trillion, compared with just $35 billion in external USD bonds. In addition, concerns about the depreciation of the Chinese yuan against the US dollar have also encouraged Chinese companies to issue debt locally rather than on the USD market. This shift to local financing reduces reliance on international capital markets, further dampening new external bond issuance activity.

Impact of lower US interest rates on new issues

The US Federal Reserve's expected rate cut should exert a significant influence on bond issuance for the remainder of 2024. With the Fed's reversal to lower rates, companies in emerging countries are likely to seize the opportunity to lock in more favorable borrowing costs in the USD-denominated debt markets. This should lead to increased issuance, particularly by higher-rated companies seeking to refinance previously accumulated debt in a higher-rate environment.

Early data for September 2024 already shows a strong uptick, with EM issuers collectively raising more than $50 billion (the highest monthly total this

year), indicating that companies are eager to take advantage of improving market conditions. For companies classified as speculative, which had been sidelined by high rates and risk aversion in the first half of the year, the Federal Reserve's easing policy could provide much-needed access to the market.

In addition, as investors seek higher yields at a time when US Treasury yields are falling, the corporate EMs sector should attract more capital flows. This dynamic should particularly benefit issuers in Latin America and Asia, where latent financing demand is already present. J.P. Morgan estimates that EM corporate bond issuance could exceed $340 billion for the year, marking a significant recovery from the reduced activity of the first part of the year.

Conclusion

In 2024, the primary EM bond market evolved rapidly, driven by a mix of global monetary reversals, local market conditions and investor sentiment. As the Fed's cut in US rates offers better issuance conditions, emerging market companies are beginning to exploit the opportunity to access international capital markets, particularly in those parts of the world where local rates remain high. Turkey's breakthrough into the emerging bond issuance market highlights the impact of rate differentials, while China's shift towards domestic financing testifies to the internal transformation underway in the world's second-largest economy.

As demand for yield grows across bond markets, and approaches to risk become more nuanced, emerging market companies are adapting their strategies to optimize capital raising in a dynamic environment. The potential for a strong issuance pipeline remains strong, and 2024 could be a pivotal year for emerging market corporate credit (J.P. Morgan forecasts a significant upturn in issuance levels). Despite the peak in issuance, market dynamics remain favorable in terms of net financing positions and investor appetite. The combination of macroeconomic factors, market sentiment and issuers' strategic actions will continue to define the market's trajectory, as it navigates between opportunities and uncertainties in the months ahead.

IVO Capital Partners' emerging bond funds have historically participated actively in the primary market. New issues offer interesting investment opportunities and improve the fundamentals of existing portfolio positions. Our management team continuously reviews new primary issues, whether from established issuers or new players. In addition, although interest rates remain relatively high, the ability of issuers to refinance at lower interest levels can have a positive impact on our portfolio, particularly when the funds are used to refinance existing debt we already hold ("call option" or "tender"), or to strengthen the credit profile of issuers.

Disclaimer: All data presented in this note are from IVO Capital Partners as at 20/09/2024. All investments entail risks, including the risk of capital loss. Returns shown are not a guarantee of future performance.