Focus on one of IVO Capital Partners' preferred sectors: infrastructure

Infrastructures have specific characteristics that make them a stable and resilient sector of activity and investment, both in clear weather and during economic downturns. Companies in this sector demonstrated their resilience during COVID 19; their post-COVID rebound has only confirmed the strength of this investment sector for bond funds."

Emma Otmani, CFA, Analyst at IVO Capital Partners

IVO Capital Partners' long-term view of the infrastructure sector

- Companies benefiting from tangible assets, essential to the economic development of their countries

- Revenues generally in hard currencies, high EBITDA margins and predictable cash flows

- Long-term concessions that expire beyond bond maturity

- Protective covenants and amortizable structures

What's behind the term "infrastructure"?

This sector comprises companies operating tangible assets under long-term concession contracts. Infrastructure investment in emerging countries contributes to their economic and social development. These investments are therefore in line with the UN's Goal 9 for sustainable development: "build resilient infrastructure, promote inclusive and sustainable industrialization, and foster innovation". This sector includes international players operating ports, airports and freeways. These companies are owned by strong strategic shareholders who are experts in their sector. For example, the Turkish company TAV Airports, which operates 15 airports in the CEEMEA region, is 46% owned by the Aéroports de Paris group, itself 51% owned by the French government.

How does this sector differ from others? Diversification, resistance and resilience

Emerging corporate bonds in the infrastructure sector offer geographic and sector diversification in bond portfolios. These companies generate revenues generally in hard currency, making them a key attraction for investors, protected from reversals and local currency devaluation in regions of the world with high economic and political risks. What's more, these companies benefit from predictable cash flows and high EBITDA margins (over 50% on average), underlining their resilience during an economic downturn. In 2020-21, the infrastructure sector was particularly hard hit by the sharp drop in international travel and the general downturn in the global economy. Nevertheless, the sector held up well during this global economic contraction, thanks in particular to high EBITDA margins, which enabled companies to rapidly rebuild their cash flow and reduce their debt leverage. They thus emerged from this period having demonstrated their ability to wait, to be resilient and to bounce back.

What's more, since debt maturities are long-standing and staggered over time, companies in this sector have approached the health crisis with greater serenity than others, and have generally not been concerned by immediate financial liquidity issues. A company can have assets operating in a country whose financial situation is deteriorating, and still generate substantial profits uncorrelated with the sovereign. The example of Ecuador is telling: while the Ecuadorian sovereign had to restructure its bond debt in 2020, the company Quiport, operator of Quito airport, continues to service its debt. However, the rating agencies cap Quiport's rating one notch above that of the sovereign. For Moody's, the sovereign cap therefore reduces Quiport's intrinsic rating from BBB- to a final rating of CCC, a difference of 8 notches. At IVO Capital Partners, we call this the zip code effect: a healthy asset in a risky country.

What special financial features characterize the sector?

The infrastructure sector is made up of companies with long-term concession contracts guaranteeing a legal operating framework, and expiring beyond the maturity of their bonds. In addition, some of these companies can benefit from amortizable structures that enable them to repay their debt over the life of the bond. This arrangement reduces the risk of refinancing at bond maturity, and proves advantageous in periods of high interest rates, when refinancing via international markets is not accessible for certain companies.

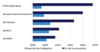

Examples of international airport concession terminations vs. bond maturity

Source: IVO Capital Partners at 15/01/2024

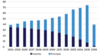

Amortization schedule for a port in Turkey - LimakPort 9.5% 2036

Source: IVO Capital Partners at 15/01/2024

Some bonds may also include a set of constraints in their prospectus, known as "covenants", offering creditors an additional safety net. Among other things, these covenants can limit the payment of dividends and the issuance of new debt.

Another aspect of financial structuring that makes this sector so attractive are structural arrangements that provide creditors with additional guarantees in situations where investors may be wary of the political or geographical context. These financial vehicles are designed to capture cash flows and isolate them from the rest of the company. This reduces exposure to sovereign debt and political reversals. Aeropuertos Argentina 2000's bonds, for example, benefit from an offshore reserve account domiciled in New York, which captures cash flows first in order to service the dollar-denominated debt; the risk of being impacted by a sudden change in monetary policy is thus reduced.

IVO Capital Partners has made infrastructure one of its preferred sectors, with IVO funds overweighted relative to the benchmark. In particular, infrastructure accounts for 16.2% of our flagship IVO Fixed Income fund, with a gross average worst-case yield in dollars of 8.9% and an average duration of 5.9. As this defensive sector is not represented in European high yield, it offers an additional source of diversification.