Focus on Mexico - Impact of the 2024 presidential elections

Impact of the 2024 presidential elections

Following the presidential election of June 2, which saw Claudia Sheinbaum become Mexico's new president, the much larger-than-expected victory of Morena and its allies, and the prospect of a qualified majority in Congress - paving the way for potential constitutional amendments desired by AMLO - have disrupted the calm seen on financial markets in recent months. Up until then, valuations had reflected expectations of a certain balance of power. However, the preliminary results seem to crystallize AMLO's desire for a one-party state, which is likely to increase market volatility in the weeks ahead and drive up borrowing costs for the Mexican state, at least in the short term, while awaiting further details on the new government's composition, fiscal policy and support for Pemex.

Sheinbaum's victory speech, however, followed in the footsteps of his campaign, emphasizing the importance of foreign direct investment in the context of the nearshoring boom, fiscal discipline, the autonomy of Mexico's central bank, and the promotion of renewable energies - themes that are dear to investors' hearts.

Marin Bourgeois

Senior Analyst at IVO Capital Partners

IVO Capital Partners' view of Mexico

- Continuity, but at what price? - The broad outlines of AMLO's mandate are set to continue under Claudia Sheinbaum, with further increases in the minimum wage, social and infrastructure programs, and support for state enterprises. However, the new administration will have to deal with an increasingly restricted fiscal space and make choices between social spending and support for Pemex.

- Towards a more constructive relationship with the private sector - Claudia Sheinbaum tends to distance herself from the outgoing president by calling for public and private capital to be brought together through "co-investment" vehicles to finance energy and infrastructure projects, which could give new impetus to nearshoring, notably through the decarbonization of the country's energy matrix.

- The spectre of a qualified majority in Congress, a risk that has been underestimated - The main identified risk of the election, the prospects of a two-thirds majority in both legislative chambers - enabling constitutional revisions - could materialize against polling expectations and should increase uncertainty in the coming months.

- The broad outlines of AMLO's mandate are set to continue, with further increases in the minimum wage, social and infrastructure programs and support for state-owned companies, despite a more limited fiscal space.

Claudia Sheinbaum, a Mexican scientist specializing in energy efficiency, won the election with 59% of the vote. She is a former mayor of Mexico City, and is in line with the policies pursued by President Lopez Obrador since 2018. Benefiting from the outgoing president's popularity, she has focused her campaign on continuing the social reforms initiated under the outgoing government, with in particular the development of welfare benefits and an increase in the minimum wage: the latter has risen from MXN 2,652 ($156) per month in 2018 to MXN 7,468 ($441) in 2024, placing Mexico in 6th place to date in South America, helping to reduce the number of Mexicans living below the poverty line from 52 to 47 million according to national statistics. Like her predecessor, who led major infrastructure projects, especially in the south of the country, such as the MAYA train ($28 billion) in the Yucatan peninsula, and sometimes economically questionable projects like the construction of the Dos Bocas refinery ($16 billion), Claudia Sheinbaum also plans to continue or initiate major infrastructure modernization projects, at a time when the country is suffering from a crying lack of infrastructure. Finally, Finance Minister Rogelio Ramirez de la O, whom Sheinbaum would consider reappointing to the post if he wins, recently stated that the government would continue to support Pemex financially.

Mexico is a historically fiscally responsible country, and AMLO proved to be a very conservative president during the COVID period: spending remained measured, unlike other countries which spent lavishly during the two years of the pandemic. In addition, the country maintained an orthodox monetary policy with largely positive real interest rates: In fact, BANXICO was one of the first central banks in the world to raise interest rates after COVID. Moreover, the country's external position is very solid, with a current account deficit well below the average for emerging countries, easily financed by foreign direct investment and remittances from nationals abroad, which the country maintains at a high level.

Claudia Sheinbaum has no plans to deviate from this fiscal and monetary line. In her words, she will continue to advance Mexico's social policy and invest in major infrastructure projects, while maintaining a responsible fiscal approach. She defends her future budgetary choices in these terms: "there will be sufficient funds for future social programs and for the projects we have proposed (...) there will be sensitivity in the use of public funds".

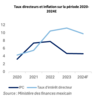

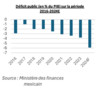

Nevertheless, the new administration will face immediate economic challenges. In particular, public spending is set to accelerate in 2024, with the presidential elections in sight. The deficit is forecast at -5.9% by the Ministry of Finance, the highest since the 1980s, exacerbating the dynamics of Mexico's public debt. For her part, Claudia Sheinbaum remained vague about her tax plans. She dismissed the idea of any far-reaching tax reform, asserting that she would increase public revenues by optimizing the efficiency of tax collection. However, this is unlikely to be enough to stabilize the public debt-to-GDP ratio during the next presidential term, which could jeopardize the country's sovereign debt rating in the medium term. The limited fiscal room for maneuver means that support for Pemex will probably be reduced, in favor of social programs.

Nearshoring, a major challenge for the country's economic future - towards greater participation by private players in key investments for the country's attractiveness under Sheinbaum

Since 2022, the Mexican economy has tended to surprise investors on the upside, supported by the phenomenon of relocation of American and foreign production chains, also known as "nearshoring". Beyond its obvious geographical proximity to the United States and the existence of trade agreements for over 30 years that offer a stable framework for investment - NAFTA, relabeled USMCA in its most recent version and which increases the requirements for locally produced content to benefit from tax advantages - the country has so far been able to capitalize on a conjunction of several factors that have reshuffled the cards in global supply chains.

Firstly, the country has been able to capitalize on the eroding competitiveness of China, where labor costs have risen significantly in recent years and are now currently 19% cheaper in Mexico, according to consulting firm Novalink, despite the dramatic increase in the minimum wage under AMLO's tenure. This difference in competitiveness has been amplified by the trade war between the US and China since 2018, which has served as a detonator with the introduction of numerous tariffs between the two countries (US tariffs on Chinese exports increased from 3.1% in January 2018 to 19.3% in January 2023) as well as multiple disruptions and shortages, such as the rising cost of shipping between the US and China. The Freightos index for 40-foot containers shows that freight rates between China and the US West Coast have soared by +212% since the beginning of the year to the end of May.

The nearshoring phenomenon, still in its infancy two years ago, is beginning to make its mark on the Mexican economy. Mexico recently became the United States' leading trading partner and main exporter, ahead of Canada and China. Investment by the public and private sectors is on the rise and has been a major driver of the higher growth Mexico has seen in recent quarters (before the normalization observed in the first few months of 2024), accounting for almost 25% of GDP, the highest share in over 20 years. Finally, foreign direct investment reached record levels in 2023 ($36 bn), with companies already present in Mexico for years investing to expand their activities, while the share of new investments in foreign direct investment is set to grow significantly following the announcement of several large projects, such as Tesla's Gigafactory - a project estimated at $5 bn.

The new administration will face the challenge of implementing the structural reforms needed to take full advantage of this new relocation strategy, after years of under-investment by the private sector in energy, mainly due to AMLO's statist energy policies and a still significant lack of infrastructure supporting the nearshoring theme in particular. Claudia Sheinbaum's proposals tend to distance herself from those of the current president, calling for public and private capital to be brought together through co-investment vehicles to finance energy and infrastructure projects, without giving further details. Among the major projects on the candidate's agenda is a plan to invest $13.6 billion between now and 2030 to finance the country's electrical infrastructure, with an emphasis on energy transition, at a time when the country is in dire need of decarbonizing its energy mix to better meet the needs of industrialists setting up in the country.

Elections in the USA will inevitably have an impact on nearshoring dynamics, particularly in the run-up to the USMCA renegotiation period starting in 2026. The US may be tempted to introduce more restrictive regulations, while Mexico is gradually becoming a platform for Chinese companies wishing to export to the US.

The spectre of a qualified majority, the greatest uncertainty of the election, seems to be materializing and has fuelled volatility on the financial markets.

During the June 2 elections, Mexicans also voted for Congress, as well as for governors and mayors; no fewer than 20,375 political mandates were renewed on this occasion. While AMLO has governed the country with a simple majority in both chambers in recent years, which has enabled him to control the budget and pass secondary legislation without being able to amend the Mexican constitution, preliminary results reveal that, against all expectations, Morena and his coalition are on course to win a qualified majority in the Chamber of Deputies and come very close in the Senate.

Morena and its allies may be tempted to approach the social-democratic MC party - an outsider in the presidential elections with 10% of the vote - in order to advance an agenda that could include constitutional amendments that President AMLO has been unable to deliver during his six-year term. Especially as the social-democratic MC party has flirted with Morena in Congress during the current sessions, suggesting a material risk of alliance in the next administration. This could allow the ruling party to go ahead with AMLO's 20 proposals to amend the Mexican Constitution, and thus reverse, among other things, the 2014 reform to liberalize energy markets, reduce the independence of the Supreme Court and electoral authorities, and eliminate certain regulators.

It should also be noted that the outgoing president would also have a few weeks to pass legislation he was unable to pass with a simple majority, between September 1 - when the new congress takes office - and Claudia Sheinbaum's inauguration in October.

The universe of Mexican corporates is, on the whole, well equipped to ward off the volatility emanating from the election, notably due to low leverage and sufficient liquidity to cope with upcoming maturities and refinancing risk. Mexico is the 3rd largest destination for investments in our IVO Fixed Income fund, representing 6.9% of the fund for a worst-case yield of 11.0% in dollars. We are particularly attracted to bonds issued by companies with tangible assets, operating mainly in the industrial and data center sectors, which account for 36% and 32% respectively of our exposure to Mexico and benefit directly from the nearshoring dynamic.

*Nearshoring: this involves relocating an economic activity to a nearby area, either another region or a neighboring country, in order to benefit from productivity gains without suffering the hazards of offshoring. Typically, the loss of interest in offshoring to Asia (and particularly China) has led to relocations to Central and South America; Mexico is benefiting fully from this offshoring movement.

*UMSCA: Free trade agreement signed in 2018 between the United States, Mexico and Canada; it follows on from NAFTA.

Sources: IEA, AFP, Bloomberg, JP Morgan, IVO Capital Partners, The US-China Business Council, la presse.ca, le Monde le Figaro.fr https://www.cairn.info/revue-pouvoirs-2019-4-page-141.htm, Mexican Ministry of Finance, Peterson Institute for International Economics (PIIE)