Focus on ESG in South America, a territory with multiple resources

Home to 6% of the world's population on 12% of its land surface, South America is a continent with its own particularities, whose ambition is to play a major role in the economy of the 21st century. However, this self-evident statement masks considerable disparities: vastness of space, diversity of climates, alternating political systems, all of which make this a complex territory. The energy challenge is huge, and climate change is particularly perceptible in LATAM. Nevertheless, the continent has everything it takes to play a major role in the renewable energy sector, and is home to some of the cleanest countries in the world when it comes to electricity: 60% of the region's electricity generation is renewable (twice the world average). In Brazil, Argentina, Mexico and Chile, solar and wind power yields are among the best, and the continent exports biofuels. Nevertheless, oil and gas-producing countries are largely dependent on revenues generated by the export of black gold. How is South America preparing to meet the challenge of the energy transition? An update on the situation to date, halfway between dependence on fossil fuels and concrete advances in renewable energies.

Mathieu Quenechdu,

ESG Analyst at IVO Capital Partners

IVO Capital Partners' long-term view of LATAM's energy sector

- An area extremely rich in natural resources: both fossil and renewable energies

- Proactive policies that define the green sectors needed to align with the Paris Agreements

- Strategic diversification of Oil & Gas players

- A renewable energy sector with very low operating costs (OPEX)

Fossil fuel production & consumption - LATAM

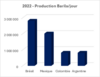

South America is home to 15% of the world's oil & gas resources. These fossil fuels play a major role in the development of Brazil and Mexico in particular, at a time when global demand is still unabated. In addition to exporting raw materials, LATAM countries also consume part of their production, mainly for transport and industry.

The 4 major oil-producing countries - Brazil, Colombia, Mexico and Argentina - each have a major public player in the oil sector. While three of these countries demonstrate a common desire to improve their emissions from fossil fuel production, things are more complex in Mexico, where the state-owned Pemex has the highest level of indebtedness in the oil sector; it has been unable to reduce its greenhouse gas (GHG) emissions, notably due to a lack of investment in its operating infrastructure. In Brazil, Petrobras leads the way and exploits its resources, mainly offshore. Petrobras has reduced its emissions by 23% in the space of a year, and is still the least polluting company per barrel in Latin America. This is also the case for Argentina's national oil company YPF, whose efforts to reduce emissions have proved significant, with a 28% drop in greenhouse gases in 1 year, and a significant reduction in carbon intensity per barrel produced. In Colombia, Ecopetrol reduced its emissions by just 2% in 1 year. In addition to their efforts to reduce GHG emissions, these companies are also committed to energy diversification. Petrobras invests $11.5 billion a year in capex in decarbonization and low-carbon energies, as well as in R&D. The company finances projects in offshore wind power, hydrogen and carbon capture. Ecopetrol, for its part, is involved in the construction of green hydrogen power plants, and expects to invest around $2.7 billion in energy transition by 2024. YPF is financing investments in wind power, the development of which is a major alternative for Argentina.

The trend towards a growing proportion of renewable energies is well and truly underway, and it includes state-owned companies in this challenge.

The region's renewable energy resources

The South American territory is made up of a wide variety of zones, most of which benefit from water resources, increasing sunshine or strong winds. Electricity is traditionally supplied by hydroelectricity (the dominant source: 45% of the region's electricity supply), coal and gas; biofuel, a Brazilian peculiarity, supplies part of the needs of road transport. In the north of Brazil, the solar potential is substantial and the location is ideal for wind power projects, thanks to the permanent trade winds. The Colombian lands are not to be outdone: their location in the equatorial zone and the diversity of climatic conditions are all assets for reinforcing the country's energy diversification.

While renewable energies already account for 1/3 of the South American energy mix, LATAM countries still have immense potential for renewing their energy production, and investments in this area are all the more attractive as LATAM countries offer long-term contracts (known as PPAs), which provide investors with income over long periods. Generally speaking, LATAM countries are working in the same direction, with a clear objective: to mitigate climate change. Achieving this goal is based on increasing the use of renewable energies and improving energy efficiency in high-emission industries. The targets announced are ambitious for a developing country: Brazil is aiming for a 53% reduction in greenhouse gases by 2030 (since 2005), and carbon neutrality by 2050, as is Colombia. Achieving them will require colossal investments, on the order of 150 billion USD.

Last but not least, South America's subsoil abounds in the rare metals essential to so-called green technologies: 50% of the world's lithium reserves and 40% of the world's copper reserves are located on the continent.

What concrete investments are already underway?

The deregulation of the El Nino and La Nina phenomena is having dramatic consequences in Central and South America. Floods in Peru and Ecuador, droughts in Colombia and the drying up of the Amazon rainforest are just some of the manifestations of climate disruption that are making themselves felt, and attesting to the increased physical risk in the region. In recent LATAM elections, the majority of candidates (with the exception of Argentina) have been left-wing parties, supporting social projects in line with more sustainable development.

State-owned oil companies are well aware of this: Petrobras and Ecopetrol are investing part of their profits in renewable energies. In Brazil, Prumo is developing offshore wind power to supply Porto de Açu, South America's largest industrial port complex. This key center is both vital for Brazilian exports and for the activity it generates in the northern state of Rio. Specialized companies are also beginning to emerge: the Guatemalan company CMI is investing in hydroelectric, wind and solar power, and CMI is offering green bonds* to finance the development of these activities.

However, South America still faces the problem of deforestation and its ravages. Energy production is not exempt from harm, even if deforestation has been halved by 2023 thanks to the joint efforts of the Brazilian authorities and private players. To preserve the Amazon rainforest and develop this impoverished region, home to 28 million inhabitants, initiatives such as the Amazon Fund have been set up. Other reforestation projects involve private companies: Suzano, a pulp and paper company, is carrying out a huge reforestation project covering 4 million hectares (the size of Switzerland) in partnership with other companies, such as Vale. The benefits are numerous for the Amazon and other parts of the continent, and contribute de facto to the protection of animal and plant species. The integration of ESG criteria is exerting positive pressure on the energy sector, distinguishing on the one hand those players committed to an overall responsible approach, and on the other those projects with the most measured ecological impact (significant reduction in GHG emissions). In addition, legal action against major corporations for environmental damage is on the increase, in tandem with the growth of litigation funds.

The energy transition requires major investments, and this is an opportunity for sustainable funds. Investments in this area at LATAM have tripled since 2019, and capital requirements are substantial. In 2023, taxonomies* inspired by the European model have been put in place to define which economic activities are considered sustainable, and highlight the sectors needed for the energy transition. Our IVO Short Duration SRI fund holds green bonds (11.5% of the portfolio as at 17/03/2024), notably issued by CMI, and we are keeping a close eye on future issues, some of which will offer interesting opportunities for our investors by combining financial returns with environmental impact.

*Taxonomy = a set of criteria for assessing the environmental contribution of economic activities.

*Green bonds = these are bonds offered on the financial market, dedicated to the sustainable sector and whose destination is perfectly pre-defined and non-modifiable.

The sources of the figures and graphs used in this document are the International Energy Agency (www.iea.com), BTG Pactual, datamondiales.com, and esgnews.com.