A changing economy, calling for massive financing from the private sector and international investors

In terms of both population and economy, India stands apart from the rest of the world. Its population has doubled in 20 years, and will reach 1.46 billion by the end of this year. This makes it a serious competitor for China, in an ambiguous relationship halfway between global competition and geo-economic alliance; the political divide, for its part, is assumed and only occasionally comes into play. When it comes to economic profitability, both India and China play the pragmatism card. In India, everything is always multiplied, and the country faces a modern-day challenge: how to combine population growth, economic growth and growing energy needs on this scale.

Qi Hang Zhao,

Analyst at IVO Capital Partners,

IVO Capital Partners' long-term view

- LEGISLATIVE ELECTIONS - The elections are expected to reappoint Narendra Modi as Prime Minister and ensure continuity in the country's economic strategy.

- INDIAN ECONOMY - India's economic turnaround over the last ten years is proving to be a winner: the country has made enormous progress in terms of macro-stability, has considerably reduced its deficits (notably by rebalancing its trade balance) and its GDP continues to grow. Today, India is seen as a stable and attractive location, thanks in part to its large, skilled workforce, which is attracting manufacturing sectors and supply chains looking to divest from China.

- OUTLOOK - The government has invested heavily during Narendra Modi's two terms in office (2014-2024); central debt has risen and he no longer has any room for maneuver; future investments must be financed by the domestic and foreign private sector, which has substantial resources at its disposal.

- OPPORTUNITIES - India offers investment opportunities in key sectors of the economy: infrastructure (ports and airports) and renewable energies. These have become attractive sectors, responding to the necessary mutation of the global economy.

Legislative elections 2024: a probable continuity of power

A legacy of British colonization, India functions as a federal republic and has adopted the British parliamentary system: the head of state has only a ceremonial role, while the head of government exercises power. At the same time, India operates a federal system of government for its 28 states, like the USA. The House of the People (the Indian Parliament) is elected by direct universal suffrage for a 5-year term. It is the renewal of this chamber that will take the entire population to the polls over the two months from April 19 to June 1.

These elections do not augur political upheaval. Running for re-election, Narendra Modi is a member of the Bharatiya Janata Party (BJP) and has been India's Prime Minister for 10 years. Once again this year, he is expected to win, and India's growth over the last decade is to his credit, driven in part by his commitment to structural reform.

The Indian economy: a proposition made attractive by macro-stability, investment and reduced deficits

Following independence in 1947, India observed the Soviet development model with interest, and in turn adopted a planning system that continues to this day. The 1990s marked a shift towards a more liberal economic policy, with the aim of increasing global trade. The Indian economy is dominated by the service sector, which will account for 63% of GDP in 2022, followed by industry (22%) and agriculture (15%).

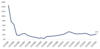

Once vulnerable, the India of the 2020s has become the 5th world power. The growth forecast for 2024 is 6.4%, underpinned by strong domestic demand; inflation, after several years of sharp rises, should be under control at around 4%. Narendra Modi's presidency has contributed to this positive turnaround, as shown by the trend in growth and debt over the past ten years.

India's GDP growth

In addition, the strength of its foreign exchange reserve accounts relative to its short-term debt, and the diversity of its financing sources, mitigate the country's exposure to external shocks.

India absorbs between 10 and 12 million new entrants to the labor market every year; this English-speaking workforce is relatively well educated, which facilitates the internationalization of the Indian offer. In addition, India promotes "Made in India" and draws attention to its attractiveness thanks to its competitive workforce: the average wage in India is $181/month, compared with around $1,050 in China.

This is both an opportunity and a constantly renewed economic challenge, which also stimulates the development of infrastructure and public services to meet domestic demand. Domestic consumption is a major contributor to growth, and the emergence of an Indian middle class is part of the equation.

Current outlook: The financing of growth must evolve in favor of private and foreign investors in order to take over from state investment.

Until now, India's growth and development have been financed mainly by the government and the state; public debt has risen from 65% to 86% in ten years.

It is now up to the private sector and foreign investors to take up the baton and finance the second phase of the country's growth. India's private sector has a low level of debt compared with other countries, and has the capacity to respond to the government's call for investment.

Structural investment has become a priority, and the government is driving this transformation by encouraging private and foreign investment. The National Infrastructure Pipeline (NIP) provides for the injection of $1,200 billion between 2020 and 2025, for the modernization of infrastructure in various sectors. Also since 2020, the Production Linked Incentives (PLI) has been promoting domestic manufacturing, from solar panels to workshops.

Narendra Modi's next term in office is likely to be marked by major investment in infrastructure to stimulate growth and continue to attract international investors, who have lost interest in China.

Opportunities: Towards a profound transformation of energy sources

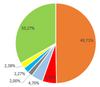

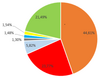

India is now the world's 3rd largest energy consumer, and its consumption has doubled in 20 years. India is heavily dependent on coal, both for consumption (44% of the energy mix in 2021) and for export. Half of the country's energy production is coal-fired, and the country exports part of this energy in US dollars, which helps to support its trade balance. National gas consumption, on the other hand, is very low, at around 6%. Today, India is highly dependent on fossil fuels, as shown by the total energy mix for 2021 below.

Domestic electricity generation, India, 2021

Total energy mix, India, 2021

India is making major investment plans in renewable energies, notably through joint ventures with foreign companies such as Total Energies & Adani, which have already developed infrastructure facilities in the sector. They favor solar power, which is competitive by nature (low Opex) in a large part of the country. Most of the financing for these infrastructures is in the form of green bonds.

Solar power supplied 2.38% of demand in 2021 (see domestic energy generation table), and India has high ambitions in this area, aiming for strict equality between solar and coal power generation by 2040. India's solar potential is considerable: in addition to its surface area, India is a tropical country, and regions such as Rajasthan and Kashmir offer very high solar potential. The major difficulty in India lies in energy storage: while solar energy production peaks in the middle of the day, consumption peaks at the end of the day, fuelled in particular by the use of air conditioners. The development of short-term storage batteries will therefore play a key role in India's ability to move towards a more balanced energy mix, and reduce its coal consumption.

India has become a magnet for investors, resulting in significant capital inflows and lower borrowing costs for the country, with current spreads tighter than those in Asia and Latin America. These recent positive trends are reflected in current valuations, particularly in the favorable infrastructure and utilities segments. We are finding some investment opportunities in Indian companies, such as in the infrastructure and renewable energy sectors. The Indian companies in the portfolio generally offer high EBITDA margins, clear visibility on cash generation thanks to their long-term contracts, economies of scale and geographic diversification. Most also benefit from the support of strong institutional shareholders. There is no doubt that the Indian private sector will be one of the major players in the international bond market over the next 10 to 20 years, given that the massive financing needs that accompany the transformation of India.'a country and'a économie de cette dimension, tout dans un contexte de transition énergétic transitionée. For example, our IVO Short Duration fund is exposed toé in India à 7.39%, almost half of which is in India.é in the renewable energies sector, for a USD yield of 7%.

The sources of the figures and graphs used in this document are the Reserve Bank of India, IVO CAPITAL PARTNERS, CEIC, Le Monde, the International Energy Agency (www.iea.com), Freedom House and donnéesmondiales.com