Between groundbreaking reforms and fiscal orthodoxy, the country is reaping the rewards of a well-thought-out policy over time.

After an unprecedented economic crisis in the years 2014-2017, which triggered a vast process of structural reforms, Brazilian growth over the last 3 years has exceeded expectations and initiated a reassessment of the country's potential. These good results are the fruit of the many reforms carried out over the last decade, and are reflected in GDP growth of 2.9% in 2023*. This significant growth is driven by very different sectors: agriculture, the energy industry and services. This is one of the characteristics of the Auriverde country, unique in the South American landscape.

Gabriel Loreto Moreira and Marin Bourgeois,

Analysts at IVO Capital Partners

*Source: Brazilian Institute of Geography and Statistics

IVO Capital Partners' long-term view

- A territory with hybrid economic characteristics, halfway between emerging and developed countries: a fertile playground for our active management strategy.

- Undeniable economic diversification coupled with genuine market depth in the emerging market universe, justifying our overexposure to the country.

- A capacity for modernization: one of the most reformist emerging countries in recent years

- A remarkable trade balance, making Brazil less vulnerable than other emerging countries.

Lula, a cautious and measured start to his term of office

Lula's election in 2022 was scrutinized by the financial markets, which were concerned about his interventionism. Fifteen months later, it has to be said that Lula is dealing with a more conservative Congress, and the radical measures he envisaged have not been implemented. The privatization of Eletrobras, for example, has not been called into question, even though it was one of Lula's proposals. He also wanted to drastically reduce the pump price charged by Petrobras, the state-controlled national oil giant. Although he has lowered it somewhat, it remains in line with international prices. This moderation reflects the company's determination to maintain sound governance.

Brazil's politico-economic approach therefore remains measured under Lula, as evidenced by the recent appointment of two ministers from the right. The 2024 budget, recently submitted to Congress, reflects the new fiscal framework and has been welcomed by the markets: it targets a primary fiscal deficit of 0%. Although this will be difficult to achieve(it depends, among other things, on revenues such as taxes on foreign assets), the budget demonstrates the new government's commitment to reform, in line with previous policies.

Structural reforms carried out since 2016

The years 2014-2017 were marked by a violent economic crisis in Brazil. Successive governments of all political persuasions were forced to embark on a vast process of structural reform. Under the centrist Temer, the right-wing Bolsonaro and, since 2023, Lula, governments have adopted a series of fundamental reforms designed to boost private investment. These include the capping of public spending in 2016, which has kept public debt and inflation under control. The labor market reform of 2017 has thoroughly modernized labor law, which dated back to the 1940s; it regularizes a large part of the population living on informal jobs, reduces labor costs and offers greater flexibility in contracts. Finally, the 2019 pension reform has set a minimum retirement age: 65 for men and 62 for women.

The current government is carrying out a structural tax reform, which is necessary given the complexity of the Brazilian tax system. The latter is perceived as an impediment to investment, and this far-reaching tax simplification is a strong positive signal to investors.

A country that has reduced its vulnerability to external shocks

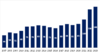

Supported by the consistency of its reforms, the country's trade balance is experiencing structural growth. This progress is mainly due to the diversity of the Brazilian economy, and to the development of the raw materials sector: the latter capitalizes in particular on the growth of investments in key sectors where the country possesses major assets.

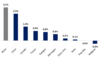

Brazil's exports in 2023

Source: Comex Stat - Brazilian Ministry of Development, Industry, Trade and Services.

Brazilian trade balance 2013-2025 (USD bn)

Sources: Brazilian Ministry of Commerce, BTG Pactual

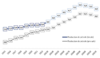

In the agricultural sector, for example, Brazil was a net importer until the 1980s. Since then, the country has significantly increased its agricultural productivity, thanks to the reforms carried out in the sector and considerable technological investment, which has helped to exploit the country's various ecosystems. The country's agricultural surplus is growing steadily, with new records set for 2023. This long-term policy guarantees a rare and envied level of food self-sufficiency.

TFP (total factor productivity) growth in agriculture - annual average

(2000-2019)

Sources: USDA, Conab, BTG Pactual

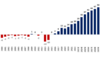

Agro-industry trade surplus

(USD bn)

Sources: USDA, Conab, BTG Pactual

In the energy sector, Brazil was an importer of oil and refined products until 2015. With a trade surplus in agro-industry (USD billion), the country also possesses considerable reserves of black gold in its waters, which it exploits at low cost via its offshore oil fields. Raw material extraction is set to grow by 80% over the next seven years. In view of the reserves identified and the development of the national oil industry, some analysts even predict that Brazilian production could become the world's 5th largest by 2028 (7th in 2023), ahead of Iraq and China.

Oil production (total and pre-salt) (Mboe/d)

Sources: EPE (Energy Research Company), BTG Pactual

Trade surplus in petroleum, distillates and petroleum products

Sources: ANP, BTG Pactual

This trend in the trade balance clearly reduces the pressure on the current account (-1.4% of GDP in 2023 or $30 billion), whose deficit is well below the average for emerging countries and easily financed by foreign investment, which the country is maintaining at high levels ($60 billion for 2023). Several indicators point to this robustness and resilience in relation to the external environment, notably international reserves amounting to $355 bn. All these major projects have consolidated the Brazilian economy, made the country more attractive to investors and demonstrated its resilience.

IVO Capital Partners specializes in investments in emerging countries, and Brazil is a favorite location for our funds: its resilience, its particularities and the efforts made over the last 20 years make it an attractive territory for our active management. Within the IVO Fixed Income fund, Brazil is our second most important investment destination (8% of the fund for a worst-case yield of 8.4% in euros). We have a particular attraction for project finance bonds (36% of our Brazilian exposure), which are generally used to finance a specific asset - in most cases infrastructure - which is collateralized, and therefore senior in the capital structure. The Brazilian universe also offers interesting opportunities for exposure to US interest-rate risk through long-dated IG/BB bonds (26% of our exposure to the country).